Market Efficiency Requires Usable Information, Not Just Disclosure

5 March 2026

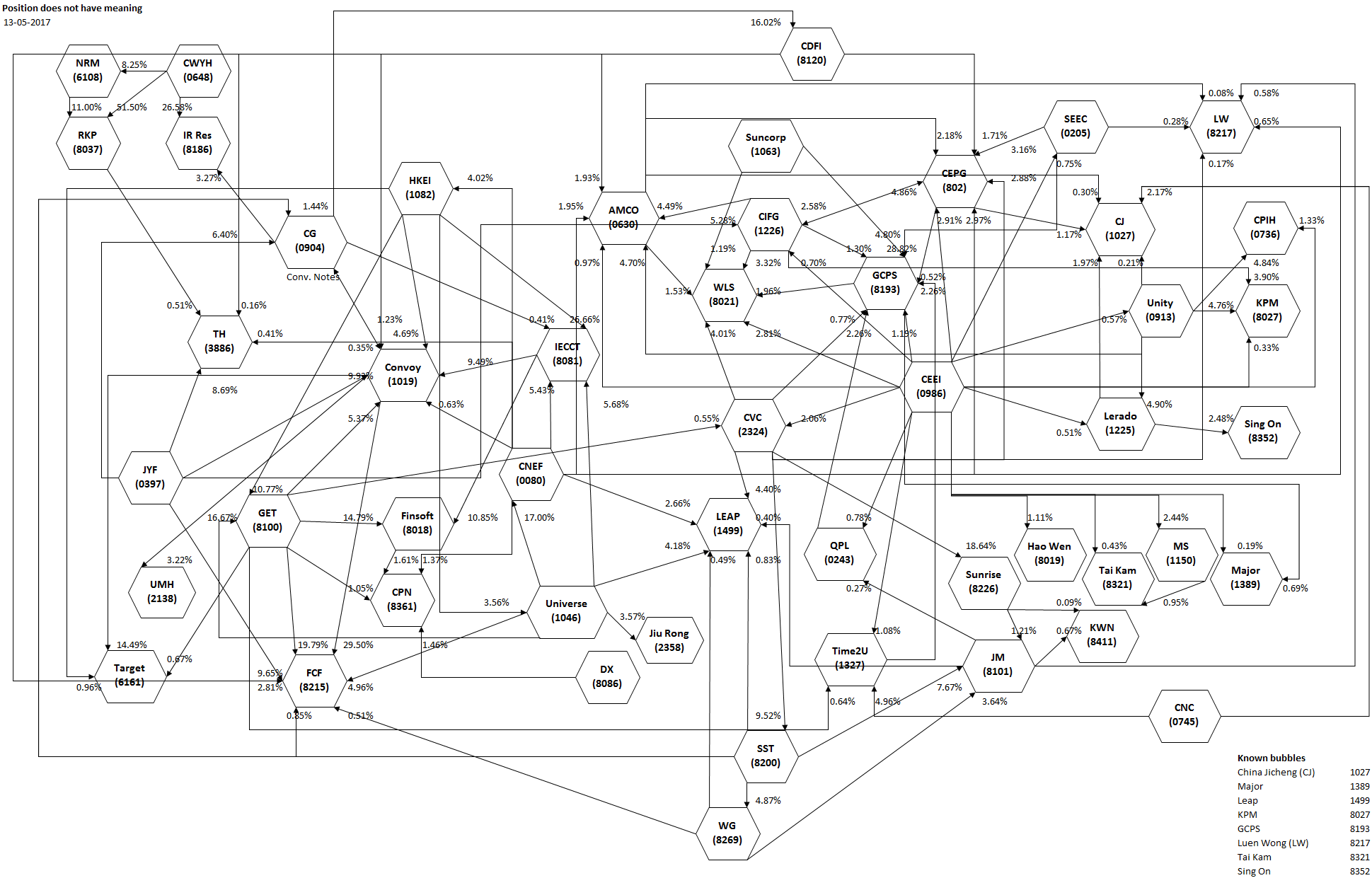

In June 2017, US$6 billion in market capitalization vanished across more than 40 Hong Kong GEM-listed companies in a large market correction. A possible theory is because a margin call could not be met by a borrower with pledged shares. Just one month earlier, investor David Webb had mapped "The Enigma Network," a complex network of cross-shareholdings among those same firms and others. Risks that were invisible to most market participants.

Nearly a decade has passed, yet the structural vulnerabilities remain largely unchanged.

These issues can be minimized through stronger disclosure rules. However, market efficiency depends not only on disclosure, but on whether information is usable.

More detailed disclosures on balance sheets and company holdings, ideally readable by computers, could have shed a brighter light on the Enigma companies.

When data is fragmented, short-lived, unstructured, or unidentifiable, information asymmetry persists despite formal transparency.

Information Asymmetry and Market Quality

Large information asymmetry creates persistent mispricing. As described in The Market for Lemons (Akerlof, 1970), when investors cannot reliably distinguish between high and low-quality firms, average valuations decline. Capital becomes more expensive even for legitimate businesses.

The mechanism is straightforward:

- Governance opacity increases perceived risk

- Risk premiums increase

- Valuations decline

- Legitimate companies face a higher cost of capital

- Lower-quality actors face weaker screening

As markets become more complex, formal disclosures do not eliminate this problem if they are not practically analyzable at scale. In many cases, even highly sophisticated actors may be impeded from reliably identifying material risks.

When the cost of acquiring and processing information is high, at best only a small subset of market participants may possess accurate assessments of firm quality. These conditions will result in an increase of uninformed traders. Arbitrage becomes risky because mispricing may persist longer than expected. As discussed in Noise Trader Risk in Financial Markets (De Long et al., 1990), rational investors may be unable to correct mispricing when they face the risk that noise traders will continue to move prices away from fundamental values. Retail investor driven securities likely magnify the problem.

Additionally primary market issuance also depends heavily on short-term expectations in the secondary market.

Case Study: The Enigma Network

A concrete example emerged in Hong Kong with the discovery of the "Enigma Network", investigated by David Webb through his platform webb-site.com.

Using his public, self-curated "Webb-site Database" (This site has an active independent continuation of Webb-site Database) and his analytical rigor, Webb mapped complex cross-shareholdings among 50 Hong Kong-listed companies. The network revealed opaque circular ownership and governance risks that were often technically public but practically undiscoverable without structured aggregation.

A month later, a sharp market correction followed. Approximately US$6 billion in GEM market capitalization was erased.

No causality is implied between the publication of the analysis and the subsequent market correction. Rather, his analysis revealed risks embedded in plain sight yet invisible to most market participants. It is difficult to argue that if these risks had been in plain sight, they would not have been more readily discovered by a larger set of investors.

Public information is not economically meaningful unless it is discoverable, linkable, and analyzable.

Structural Sources of Practical Information Asymmetry

While independent analysts like David Webb bridge the gap by synthesizing public data, market efficiency shouldn't rely solely on the herculean efforts of private actors. A healthy ecosystem requires widespread data assimilation and coordinated belief, not just isolated discovery. When third party platforms are the only ones making sense of the noise, they become vital but thin layers of protection against systemic opacity.

When trying to identify possible issues, three structural weaknesses are particularly consequential:

- Archival Fragility: The loss of historical context

- Analytical Friction: The lack of machine-readable non standardized formats

- Identity Ambiguity: The failure of unique entity resolution

Each increases due diligence costs and increases market inefficiency.

1. Archival Fragility and Institutional Amnesia

Markets price future expectations, but expectations are constructed from historical evidence.

When historical data disappears due to delistings or limited archival windows, markets suffer from institutional amnesia.

Examples include:

- CCASS data (mostly current broker/custodian holdings) is publicly accessible for only about one year. If a company delists, associated data disappears the next day. ( Official 1 year CCASS records )

- Quotation sheets appear to be available only for the current and previous month through the UI. But files stay on the server for the current year and can be accessed through date-specific file naming conventions. A one-year history is still rather sparse for long-term analysis. (As of 2026-03-02 Quotes for 2026-01-05 can still be accessed )

- There is also a risk of losing inferred data that depends on context, such as timing. Solicitors data from the Law Society of Hong Kong is point-in-time; when a solicitor is added, one needs to keep track of the time the modification was first observed, otherwise the information about appointment and retirement dates is lost. ( None of the member detail pages show appointment or resignation date. Ref)

If a company delists and associated data disappears, investors lose critical context for governance, custody, and transaction patterns. Long-term archival access is not a convenience feature. It is a structural component of market integrity.

Without persistent records

- Due diligence costs rise

- Small retail investors face higher research barriers

- Private archival actors gain disproportionate informational advantage

2. Machine Readability and Analytical Scale

Often, the constraint is not missing information but the usability of its format.

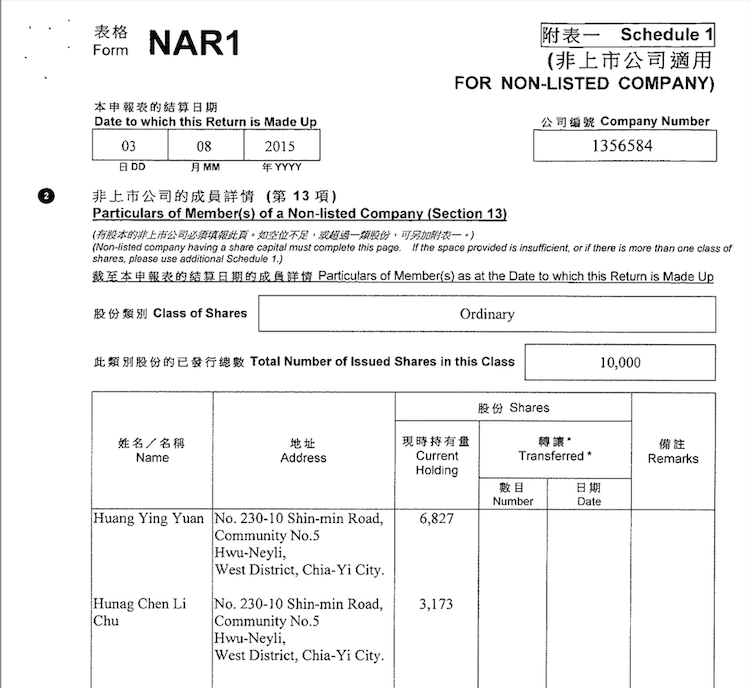

Consider Lerado Group (Holdings) Co Ltd (1225), a company connected to the Enigma network. Lerado was 19.50% owned by [Intelligence Hong Kong Group Ltd (IHK), a private company. To determine IHK ownership, an investor must purchase its Annual Return (Form NAR1) from the Companies Registry. (HKD 16 as of 2026-03-02)

The filing is provided as PDF, human-readable, but not analysis-ready. Manual review shows IHK was wholly owned by Lerado's chairman and his wife.

This works for one company, but does not scale. Finding and mapping complex networks on the Enigma scale requires reviewing hundreds or thousands of filings, each located, purchased, downloaded, and parsed manually. The cumulative time and cost become substantial.

By contrast, the UK Companies House provides corporate and beneficial ownership data through a free API, enabling automated retrieval of ownership information. What may require days or weeks of manual work can be completed in seconds.

Among many things, structured formats also allow:

- Cross-company comparison

- Automated valuation modeling (e.g., DCF, P/E aggregation)

- Director network mapping

- Accounting analysis over multiple years and companies

One possible standard, used by the US and over 60 other countries, is XBRL. HKEX filings remain PDF based, which was designed for print and serves only human reading. The SFC established an [XBRL Preparatory Working Group in 2005, with its last mention in 2006.

Machine-readable disclosure does not only benefit institutional investors. It lowers fixed analysis costs and narrows the gap between professional and retail investors.

XBRL introduces tagging complexity and compliance cost, but likely much lower than the aggregate private cost of repeated manual extraction from PDFs. Moreover, full XBRL adoption is not the only path. Other standardization, such as mandatory machine-readable tables in CSV or simply HTML, would already materially improve analytical access.

Transparency without structure preserves asymmetry and makes it harder for Hong Kong to compete with other financial hubs.

3. Identity Resolution and the Birthday Paradox

A subtler but critical constraint is weak unique identification across filings.

Since full HKID disclosure was phased out in 2021, identification of individuals often depends on name plus partial HKID (first three characters), yielding only 1,000 combinations. This solution has two major issues:

- Names are not standardized. A single individual may appear under multiple variants, with or without middle names, English names, Chinese characters, or alternative Mandarin and Cantonese transliterations ( e.g. Cheung and Zhang ).

- Even assuming perfectly consistent formatting, common names cannot guarantee uniqueness across a large population.

On 2026-01-13, the Companies Registry showed 250 records for "Chan, Chi Keung." With 1,000 possible partial-HKID combinations, the probability that at least two records share the same three-character identifier is effectively 100%.

The calculation assumes an equal distribution across the 1,000 possible HKID combinations. But any non-uniform distribution of identifiers generally increases the expected collision frequency, meaning the uniform case represents a conservative baseline.

The calculation is based on the birthday paradox, which asks for the probability that in a class of 23 students, at least two share the same birthday. The question assumes equal distributions of birthdays across the 365 days. The answer is around 50%, which seems paradoxically high to most people, giving it its name. Yet the birthday problem is not a paradox in the traditional sense but a counterintuitive mathematical fact.

Applying this to our example for $n=250$ and $d=1000$, the collision probability is 99.9999999999998%.

Admittedly, Reason 1 may lead a single person to have multiple records, making the actual number of unique people smaller than 250. This does not minimize the problem, it reinforces it through a second issue.

Even assuming just 100 unique people, the probability would still be 99.4%. For 100 people, we would expect about five matches, meaning ~10 people would share the same HKID (three digits) with someone else, which is close to the eight matches David Webb verifiably found for "Chan, Chi Keung" in 2021, when HKIDs were still fully visible.

Those are just the matches for one name, but there are many common names in Hong Kong and Mainland China.

The identity problem exists in many places, including but not limited to director appointment filings where one needs to cross-check a new director's biography to link them to the correct person.

Public-company management receives limited liability privileges in exchange for meaningful disclosure obligations to support investor due diligence.

HKIDs are not passwords but even if one accepts the belief that they should not be disclosed for security reasons, some other unique identifier would still be necessary, such as the SEC's CIK system used in the US.

When identity resolution fails, uncertainty rises and cost of capital rise with it.

The Broader Implication

Webb-site demonstrated that structured, persistent, and reconciled data can materially improve market transparency. It aimed to tackle these issues through complex automated and manual data collection, which took significant effort and resources.

Importantly, the underlying information was already public.

The value came from:

- Aggregation

- Standardization

- Historical preservation

- Identity reconciliation

If disclosure systems ensured:

- Long-term archival persistence

- Machine-readable standardized formats

- Stable unique identifiers

Then practical information asymmetry would decline significantly. Markets would not merely be more transparent in theory. They would be more efficient in practice.

Market efficiency is ultimately a function of data infrastructure. And infrastructure determines who can see risk before it is priced.

SW

References

-

Akerlof, G. A. (1970).

The market for lemons: quality uncertainty and the market mechanism. Quarterly Journal of Economics. -

De Long, J. B., Shleifer, A., Summers, L. H., & Waldmann, R. J. (1990).

Noise trader risk in financial markets.

Journal of Political Economy. -

Financial Times. (2017).

Hong Kong stocks make a mysterious $6bn plunge.

https://www.ft.com/content/f6190f45-1b48-320b-8feb-5431dbd4dd8f -

Financial Times. (2017).

Hong Kong's small-cap 'bloodbath' spills into day two.

https://www.ft.com/content/cf51c310-5bda-11e7-b553-e2df1b0c3220

-

Financial Times. (2017).

Traders seek source of Hong Kong's 'Enigma' market crash.

https://www.ft.com/content/e1db0afc-5bab-11e7-b553-e2df1b0c3220 -

Hong Kong Exchanges and Clearing (HKEX) (n.d.).

CCASS shareholding disclosure system.

Accessed: 4 Mar 2026.

https://www3.hkexnews.hk/sdw/search/searchsdw.aspx -

Hong Kong Exchanges and Clearing (HKEX) (n.d.).

Daily quotations.

Accessed: 4 March 2026.

https://www.hkex.com.hk/eng/stat/smstat/dayquot/qtn.asp -

Hong Kong Exchanges and Clearing (HKEX) (n.d.).

Daily quotations 2026-01-05.

Accessed: 4 March 2026.

https://www.hkex.com.hk/eng/stat/smstat/dayquot/d260105e.htm -

Reuters. (2020).

Hong Kong activist investor David Webb to step back for health reasons.

https://www.reuters.com/article/business/hong-kong-activist-investor-david-webb-to-step-back-for-health-reasons-idUSKBN23F0V5/ -

Securities and Futures Commission (SFC). (2005).

Annual report 2004452005: investors first.

https://www.sfc.hk/sfc/doc/EN/speeches/public/newsletter/05/may_jun05_eng.pdf -

The Law Society of Hong Kong (n.d.).

Law list 45 members with practising certificate.

Accessed: 4 March 2026.

https://www.hklawsoc.org.hk/en/Serve-the-Public/The-Law-List/Members-with-Practising-Certificate?pageIndex=1 -

UK Companies House (n.d.).

Public data API 45 persons with significant control (PSC).

Accessed: 4 March 2026.

https://developer-specs.company-information.service.gov.uk/companies-house-public-data-api/reference/persons-with-significant-control/get-corporate-entity-beneficial-owner?v=latest -

Webb Database (n.d.).

Intelligence Hong Kong Group Ltd.

Accessed: 4 March 2026.

https://webb-database.com/dbpub/orgdata.asp?p=61696 -

Webb Database (n.d.).

Lerado Group (Holdings) Co Ltd (1225).

Accessed: 4 March 2026.

https://webb-database.com/dbpub/orgdata.asp?code=1225 -

Webb, D. M. (2015).

Bubbles and troubles in Hong Kong.

Retrieved from the Internet Archive

https://web.archive.org/web/20250522224245/https://webb-site.com/articles/trouble2015.asp -

Webb, D. M. (2017).

The Enigma Network: 50 stocks not to own.

Retrieved from the Internet Archive

https://web.archive.org/web/20231203072841/https://webb-site.com/articles/enigma.asp -

Webb, D. M. (n.d.).

Webb-site repository.

Accessed: 4 March 2026.

https://drive.google.com/drive/folders/13mzAvvufXC3QmH8OvMVx2juUi7qdnVLL -

Wikipedia. (n.d.).

Information asymmetry.

Accessed: 4 March 2026.

https://en.wikipedia.org/wiki/Information_asymmetry -

Wikipedia. (n.d.).

Birthday problem.

Accessed: 4 March 2026.

https://en.wikipedia.org/wiki/Birthday_problem -

Wikipedia. (n.d.).

The market for lemons.

Accessed: 4 March 2026.

https://en.wikipedia.org/wiki/The_Market_for_Lemons

Copyright & disclaimer, Privacy policy

Webb-site.com was originally created by David M Webb MBE

We are committed to maintaining high quality and expanding the database with additional data and insight.